Connect With Your Community!

Connect With Your Community!

Just how deep do Montana's widely discussed housing affordability woes run? Newly released data from the U.S. Census Bureau sheds some statistical light on one facet of the challenge.

Housing affordability is a product of two things: how much it costs people to keep a roof over their heads, and how much income they have to pay for it. While Montana has seen ballooning housing prices in recent years, the state's population is also earning more. The census figures indicate the median monthly housing payment in 2022 was about $1,000, up from roughly $730 in 2012. Median household income, in comparison, was about $68,000 last year, up from roughly $45,000 a decade prior.

A typical rule of thumb is that "affordable" housing costs its occupants no more than 30% of their pre-tax income - say, for example, no more than $1,000 a month or $12,000 a year for a single person with an annual salary of $40,000.

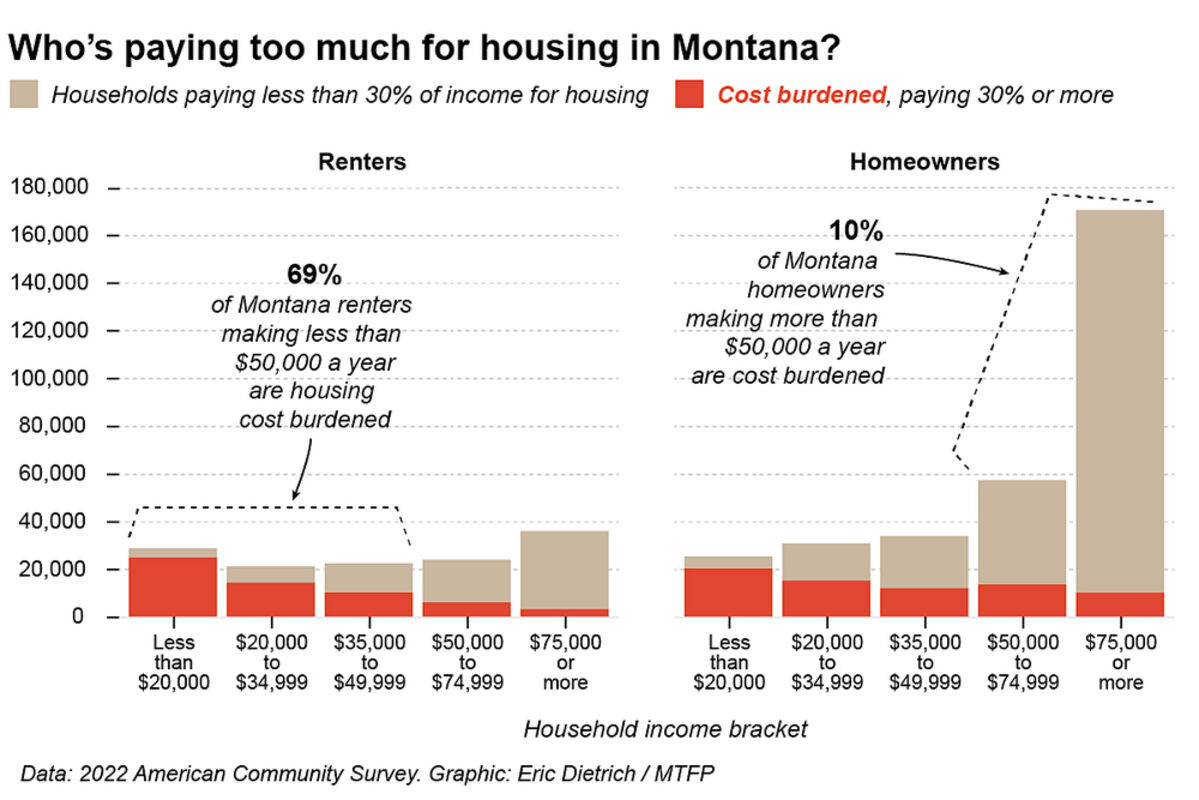

According to new data from the bureau's American Community Survey program, about 29% of Montana households were paying more than that threshold last year.

Nearly all Montana renter and owner households with incomes of $50,000 or more, 89%, re-ported housing costs below that 30%-of-income threshold. Lower-income households, in com-parison, often struggle. Of Montana renter households below the $50,000 income mark, 69% are cost-burdened with housing payments above the 30% threshold.

That percentage, which equates to approximately 71,500 households, has risen by 9 percentage points over the last decade.

Some caveats: Unlike the decennial census counts, which try to reach almost every U.S. resi-dent directly, American Community Survey numbers are based on responses from a sample of Montana's population, meaning these figures involve some degree of uncertainty.

Additionally, these numbers represent the full state, both destination communities like Bo-zeman and parts of Montana that remain comparatively affordable. They also include longtime homeowners who have either paid off their mortgages or have housing payments that reflect the lower purchase prices available to buyers in decades past.

Editor's Note: This article was originally published at http://www.montanafreepress.rog.